COVID-19 and Market Volatility

With many major market indices circling correction territory this week (defined as a pullback of at least 10% from recent highs), it is important to remind ourselves how we prepare for and respond to market volatility, especially when the market is reacting to exogenous world events with relatively unknown or indeterminate linkages to the global economy. It is practically impossible to avoid headlines related to the latest market antagonist, the coronavirus disease 2019 (COVID-19), which has grown from a concentrated outbreak in central China to a near-global pandemic.1 Obviously, the human toll from this disease, though currently limited in the scope of the global population, is most unfortunate, and we express our hope that those who have been affected will soon recover and that the spread of COVID-19 will slow to a halt. Nevertheless, in regard to the possibility that COVID-19 does become a global pandemic, we as financial professionals must rely on the expertise of those in the medical community, just as the rest of the public does, and heed the advice of our government agencies in taking precautions to protect our health at home and abroad, appreciating that this may take some time to resolve.

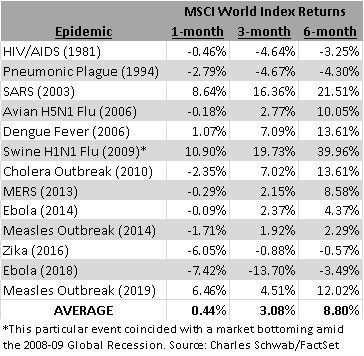

Boston Research & Management is closely monitoring the situation in financial markets as they develop and we remain confident that our portfolio positioning and style of value-focused investing is among the best strategies for long-term capital appreciation across all market and economic climates. Undoubtedly, market participants feel the spread of COVID-19 will have a negative impact on the well-being and growth of many companies, and potentially the economy, a belief that is also beginning to reflect in analysts’ and economists’ forecasts. Current estimates indicate that an anticipated recovery in earnings among S&P 500 components may fail to materialize as expected in the first half of 2020, prolonging weakness that emerged in later-2019 as the effects of trade uncertainty and geopolitical tensions on global growth began to feed through to companies’ bottom lines. Possible supply-side shocks stemming from COVID-19’s impact on industrial output in China, which is estimated to be 50% to 60% of its normal level at the moment, also loom over the market, with the potential for a spill-over into the US economy relatively unclear in this early stage. Importantly, however, history has shown that past shocks of this nature (those stemming from an outbreak of disease) failed to cause a lasting reduction in global market returns, with the MSCI World Index’s average returns positive one month, three months, and six months after the peak of prior epidemics:

Even in more severe instances of disease, such as the outbreak of H5N1 “bird flu,” MERS, and SARS, which, based on available data, all had higher mortality rates than is being currently reported for COVID-19, global equity markets quickly recovered from weakness and posted above-average gains in the following months. Of course, this time could be different and we would be remiss to ignore some of the concerns that persisted well before COVID-19 took center stage, including a flattening Treasury yield curve, slowing earnings growth, and stretched valuations. Prior to this recent volatility, BRM was proactive in managing our portfolios in light of equity markets’ very strong, perhaps overexuberant, performance, where new record highs were reached in rapid succession and the S&P’s year-to-date gains topped 4.0% through February 19, 2020, a period that included just 33 trading days. For the first time since the 2008-09 Great Recession, we took a notably more defensive position in the market, looking to protect portfolios from downside risk where appropriate, on the belief that conditions did not lend themselves well to absorbing any shocks. While we were not necessarily preparing for anything specific, such shocks came far sooner than we would have imagined, and our emphasis on reducing risk, a consistent part of our portfolio management process, has been immediately rewarded.

We also revisited our expectations for future growth, maintaining a conservative approach, well-grounded in company-specific fundamentals, that has long strengthened our portfolios in times of stress. In the past, we have avoided investments in highly cyclical sectors such as travel and discretionary retail, as well as companies with far too concentrated revenue streams in foreign countries, market components that are currently among the most negatively affected by the COVID-19 outbreak. We have also always emphasized a disciplined method of investing that avoids nearsighted, reactionary decision making when the best course of action is often to let positions stand as they are. At the same time, dislocations may create some opportunities for measured investment, which we remain on the lookout for at all times. While it is possible that the market may decline further before investors find sufficient confidence in our government’s ability (and that of other governments) to control COVID-19 and mitigate its impacts, we seek to look past the headlines, understanding that turbulent conditions can sometimes arise in the market and that investors have more recently been fortunate to enjoy an unusually smooth stretch of solid equity returns. A re-rating of expectations is not surprising at this juncture of the decade-long bull market and COVID-19 may simply be a catalyst for a cool-down that was baked into the market long ago, one that is necessary to realign conditions for sustainable, long-term growth.

![]()

________________________________________________________________________________________________________________