Keep An Eye On The Credit Market

“The rate of interest is not a narrow phenomenon . . . It affects profoundly the distribution of wealth. In short, upon its accurate adjustment depend the equitable terms of all exchange and distribution.”

Irving Fisher

The Rate of Interest

1907

It has been a rocky year for markets grappling with a Federal Reserve intent on bringing high inflation in check, dysfunction in Washington with elections around the corner, geopolitical hostilities, currency volatility, and a weakening global growth outlook. In response, equity markets moved lower in the latest quarter and remain deep in the red through the third quarter this year (S&P -24.8%; DJIA -20.9%; NASDAQ -32.4%). Those moves included both a 14% rally to start the quarter and a 17% decline to close it out (Figure 1).

All of these factors converged at the Fed’s September 21st confab, leading the central bank to hike short term interest rates by 75 basis points.1 Though such a move was to be expected following the high Consumer Price Index (CPI) report a week earlier, stocks still sold off as the Fed confirmed policy would stay restrictive indefinitely to help cool inflation. So, how might weary investors looking for an inflection point in stocks find relief? They may gain insight from an unexpected place – the bond market. This analysis focuses on bond investing. We expect stabilization of interest rates may well presage the next equity market recovery.

Bonds are issued in many shapes and sizes with a wide variety of return and performance expectations. But in today’s markets, all fixed income instruments have suffered price declines this year, regardless of their characteristics. And with each tick down in bond prices, stocks have suffered a similar fate, so we should expect stabilization of the bond market to be a prerequisite for any meaningful recovery in stocks.

How does Fed policy impact this? The most direct connection can be seen in short-term Treasury bills. Examine Figure 2 below. The Effective Fed Funds Rate2 (orange line) and the 3-month Treasury yield (light blue line) move in harmony, albeit not tick-by-tick. That’s because while the Fed only meets once every month or so to discuss its target rate policy, the Treasury market never sleeps and often anticipates the Fed’s next move.

Now examine the dark blue line – the yield on the 30-year Treasury note. You can see its moves generally shadow changes in short-term rates, but with significant differences. Why is that? The simple answer is risk. It is commonly said that Treasuries are a “risk-free” investment, meaning the US government is expected to make good on all interest payments and the return of principal upon maturity. But defining risk in a broader sense--one that includes uncertainties like unexpected changes in inflation, Fed policy, future interest rates, and the willingness of investors to lend to the US government, among others--creates space for these divergent moves.

However, should investors even care about these risks? Bonds are “boring” and “safe” right? It may have seemed that way due to the near-relentless decline in interest rates starting in the early 1980s, but that is not always the case. It may sound counterintuitive, but with fixed income instruments, falling yields mean rising prices, and vice versa.3

Figure 3 below shows the price change over the past five years for the Bloomberg US Aggregate Bond Index, which encompasses nearly the entirety of the US Investment Grade bond market. The index enjoyed strong positive returns from late 2018 through mid-2020, a period when the Fed was either cutting or maintaining short-term interest rates. Since the start of this year, however, US bond prices have suffered a sharp decline exceeding 10% as interest rates--both short and long-term--have risen. In turn, 10-year Treasury yields, a common benchmark in the fixed income world, have risen from just 1.51% at the end of 2021 to 3.73% at quarter-end.

In practice, bond investing can seem like an insurmountable task for individuals (and even some professionals), complicated by the alphabet soup of credit ratings, the jargon of “spreads” and “duration”, tax concerns, and so on. Thus, many investors find themselves in commingled Mutual Funds (often the only option in employer sponsored plans). Such funds are subject to significant prices swings, since they have no maturity date and, therefore, sometimes no near-term hope of recovery after a selloff like the one depicted above. While the diversified and/or active approach used by these Funds can be appropriate for accessing certain segments of the market, individual bond ownership has significant advantages. Steady cash flows and known maturity dates can help individuals with planned (or even unplanned) life events. Tax concerns can be catered to as well. Staggering maturities (a.k.a. a laddered approach) avoids deploying too much capital at market tops, while holding until maturity reduces concerns about interim prices movements.

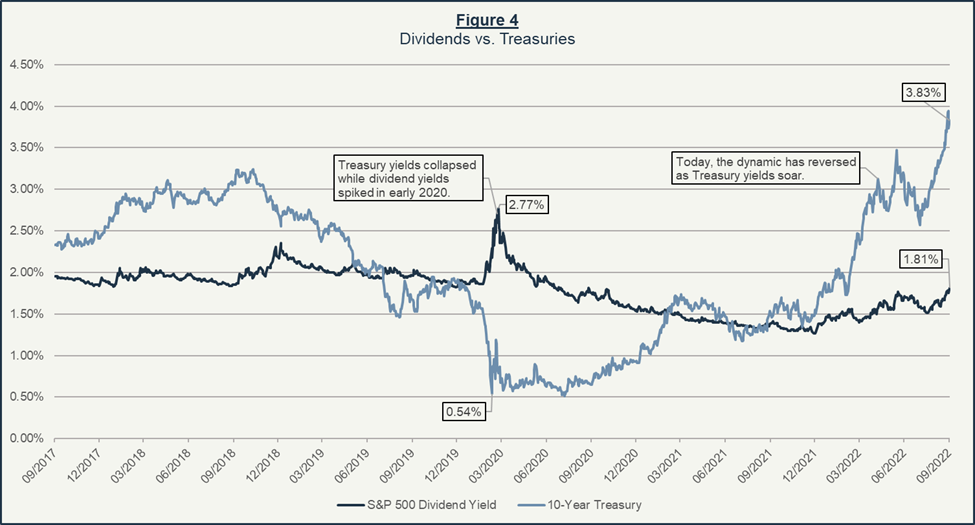

Though fixed income markets have come under pressure, it isn’t all bad news. Bond investors should be thrilled to lock in the highest rates we’ve seen in years. Bonds at their essence are income vehicles; using them for “price appreciation” is at best a speculative bet that interest rates will fall. This year’s selloff has created a long overdue alternative for income-starved investors which, ironically, is part of the reason equity prices have fallen. For much of the past several years, the dividend income earned from a broad stock portfolio has matched or even exceeded the yield on bonds. See Figure 4 below, which compares the dividend yield of the S&P 500 (dark blue line) to 10-year Treasury yields (light blue line). With stock and bond prices falling in recent months, both sources of income are on the rise, but bond yields have risen faster.

In summary, risks abound. Investors need to stay alert. A wide variety of economic and market outcomes are possible in the coming months. Stability in the bond market, if and when it should arise, might offer an early signal that a turning point in equity markets is near. And remember, times of turmoil also create opportunity, often in unexpected places.

_________________________________________________________________________________________

1 A basis point represents 1/100th of a percentage point.

2 While the Federal Open Market Committee determines the range for the Fed Funds Target Rate (the rate banks charge each other for overnight borrowing), the Effective Fed Funds Rate is calculated based on actual transactions through the program.

3 Imagine an investor buys a bond for $100 with a fixed 2% coupon and a one-year maturity. The yield on that bond would be 2%, with the original $100 principal being returned to the investor upon maturity. Then imagine one-year interest rates instantly double to 4%. That bond’s price would have to decline to about $98 so a buyer of that same bond would earn the new market rate of 4% - half from the 2% fixed coupon and half in the form of price appreciation (from $98 to $100 at maturity).