Managing Through the Cycle

If you invest only for the worst-case scenario, you will never be invested.

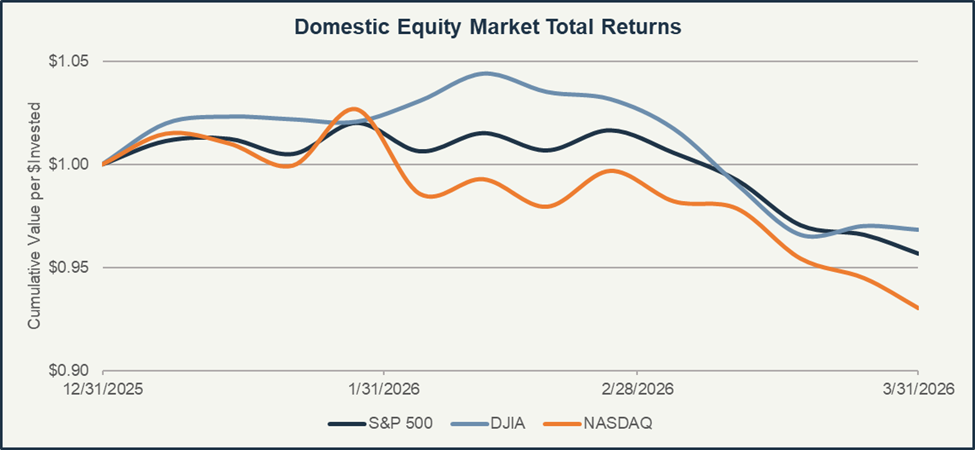

What was a slogging marathon of a quarter turned into a sprint at the end, with markets closing out the last day of Q1 2026 broadly higher and the S&P 500 posting its best single-day performance since May 2025. Yet, this finish-line performance failed to adequately reflect the challenges endured across essentially all asset classes throughout the first three months of the year and, in the end, could not entirely erase what was otherwise the market’s worst drawdown1 in nearly a year (S&P 500 -4.4%; DJIA -3.2%; Nasdaq -7.0%).

Pressure came from all sides, with headlines about war in Iran, AI disruption, and private credit woes proving particularly jarring. The defining event of the first quarter may have been the outbreak of hostilities between the U.S., Israel, and Iran in late February, which swiftly transformed from a geopolitical shock into a global energy supply disruption of historic proportions. The closure of the Strait of Hormuz, through which roughly 20% of the world's daily oil supply normally flows, sent crude prices surging above $100 per barrel for the first time since 2022. Equity markets in Europe and Asia, more heavily dependent on Gulf energy than the U.S., were particularly vulnerable, while central banks across the world were forced to contend with an inflationary shock that pushed back against a previously slow-but-steady move toward lower interest rates.

However, history suggests that markets tend to price in worst-case outcomes during geopolitical crises and then recover meaningfully once the fog begins to lift. While the major indices remain down from the start of the year, equities have repeatedly rallied on ceasefire talks, suggesting continued optimism and pent-up buying demand from investors. Whether energy markets can share in the relief remains to be seen, but key to that is the near-term resolution of hostilities in the Strait of Hormuz, rather than the longer-term outcome of the entire war. While no one desires a protracted war with Iran, resuming the free flow of oil through the Strait should be enough to induce a measure of calm across global oil markets, in turn alleviating inflationary pressures domestically. Additionally, with the word “stagflation” (a period of rising inflation paired with slowing growth) creeping back into the common vernacular, it is important to remember that the U.S. is in a much different—and more favorable—position relative to prior Middle East conflicts. Although oil supply shocks are inflationary for all economies, their impact on economic growth differs between net importers and net exporters of oil. During the 1970s (soon after the term “stagflation” was coined), the US was inherently more vulnerable to higher energy prices as a net importer of oil, which suffer stagflation as higher energy costs reduce household income and business profits. Today, the U.S. is actually a net exporter of oil (and the single largest oil producing country in the world), which has expansionary effects on the economy that offset inflation and therefore help mitigate stagflation. While the negative impact of higher energy prices on the transportation and manufacturing sectors will still flow through to the broader economy, they will not be nearly as severe as those that spurred previous crises.

Even before the war in Iran dominated headlines, artificial intelligence was already an acute source of market anxiety—not because AI was disappointing investors, but because it was working too well. Beginning in January and accelerating into February, software stocks suffered one of their worst corrections in a decade, with the S&P 500 Software Index falling nearly 25% from the start of the year through late February. The catalyst was a growing fear that AI-powered automation tools were on the verge of displacing the subscription-based software business models that had commanded premium valuations for years. The selloff was broad, driving a so-called “SaaS-pocalypse” that hit names ranging from Salesforce to Adobe, Microsoft, and many more.

However, these fears, while understandable, appear to have run well ahead of the evidence. As Morgan Stanley's investment strategists observed in March, the profits of companies perceived to have been “disrupted" by AI have largely held up, and businesses with deep proprietary data and complex enterprise integrations are proving far more resilient than the market's initial reaction implied. The more probable outcome of all this is the one that has played out across prior technology cycles: AI becomes a productivity multiplier that expands the overall market rather than simply reshuffling it. The rotation away from richly valued software names and toward industrials, financials, and infrastructure—sectors that build and power the AI economy—is a development that is likely to be both healthy and durable. The AI opportunity remains vast, and the market is simply becoming more discerning about where within that opportunity the greatest value will accrue.

The third source of market unease this quarter was the private credit sector, which swelled to an estimated $1.8 trillion market over the past decade and a half as banks pulled back from riskier lending following the 2008 financial crisis. Concern intensified after high-profile borrower collapses in late 2025, including auto-related lenders Tricolor and First Brands, raised questions about underwriting standards, valuation transparency, and liquidity, particularly in retail-facing credit vehicles like closed-end business development companies (BDCs) and interval funds. Shares of major alternative asset managers—which effectively became a liquid proxy for private credit skeptics—fell sharply, with some declining 20% to 40% from their recent highs, driven by redemption requests at several large funds that prompted managers to restrict withdrawals. The anxiety was further compounded by the aforementioned AI-related concerns about the health of software companies, which represent a meaningful share of private credit loan books.

While these concerns are undoubtedly serious, they have not risen to the level of “systemic” and appear unlikely to do so. Comparisons to the 2008-09 Financial Crisis miss key considerations, namely that, even at nearly $2 trillion, exposure to the private credit markets pales in comparison to the $10 trillion+ mortgage-backed security and derivatives market, particularly within the banking sector. Both banks and investors to a large extent are also much better capitalized than they were nearly 20 years ago, and leverage within private credit remains relatively minimal. While risks within certain corners of the economy and Wall Street may be elevated, those without exposure to private credit or similarly stressed illiquid markets should weather the storm just fine.

It is for these reasons that we have always, and will continue to, stress a balanced and diversified approach to investing designed to work through all economic and market cycles, diligently managing exposure to risk and avoiding “trendy” investments with more pronounced booms, busts, and transparency issues. Such a strategy may not capture every peak of every bull market, but it is one that has proven time and again to be the surest path to preserving and growing wealth across the inevitable uncertainty that lies ahead. And as this quarter has reminded us, that uncertainty can arrive from any direction, at any time.

_________________________________________________________________________________________

1 A drawdown is a measure of the market’s performance from its most recent peak to its most recent trough. In Q1 2026, the S&P 500 reached an intra-quarter high on January 27th before falling 9.1% through March 30th, the worst such decline since April 2025.