A Picture is Worth A Thousand Words

The greatest value of a picture is when it forces us to notice what we never expected to see.

John Tukey

American Mathematician

1915-2000

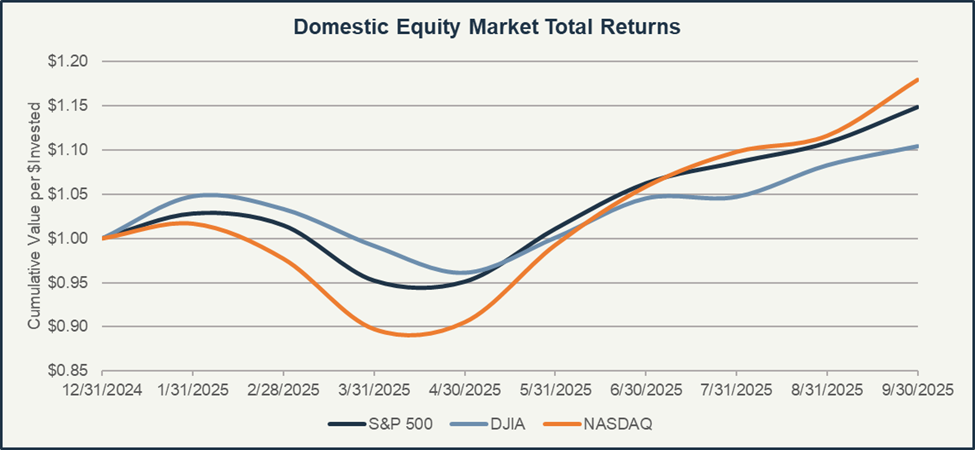

Another month, another set of all-time highs. Such has been the persistent—and often defiant—theme of equity markets throughout much of 2025. In fact, using the S&P 500 as a barometer, 6 of the last 9 months have each produced record highs for stocks. The third quarter was no exception, with the S&P, Dow, and Nasdaq all marching to new peaks in late September (S&P 500 +8.1%; DJIA +5.7%; Nasdaq +11.4%).

Yet the question of “where do we go from here” remains challenging. On one hand, underlying economic conditions remain relatively robust and supportive of further market gains. On the other, issues in terms of stock market concentration and frothiness among certain tech and AI-related names persist. Rather than add to the cacophony of pundits attempting to prophesize the market’s next move, below are a few charts and figures that we feel may help inform near-term expectations.

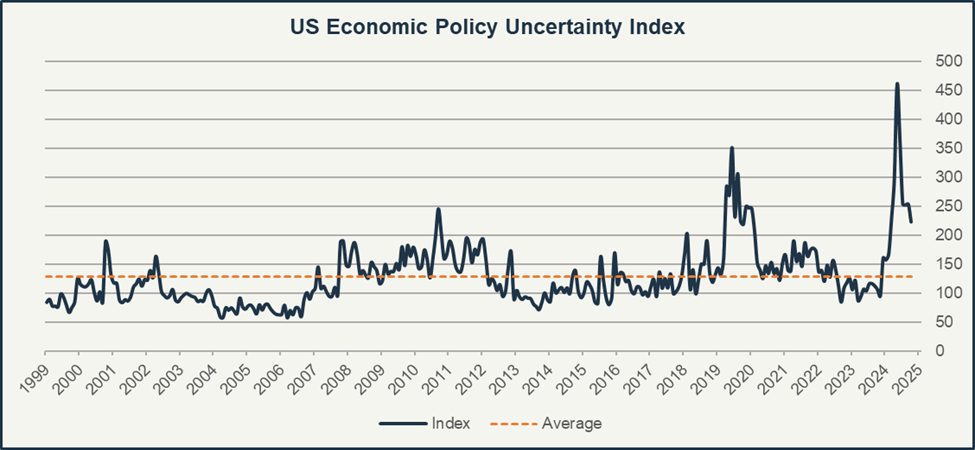

Amid the government shutdown, tariffs, and other political strife, uncertainty with regard to US economic policy remains very high, though down from peak levels earlier this year.

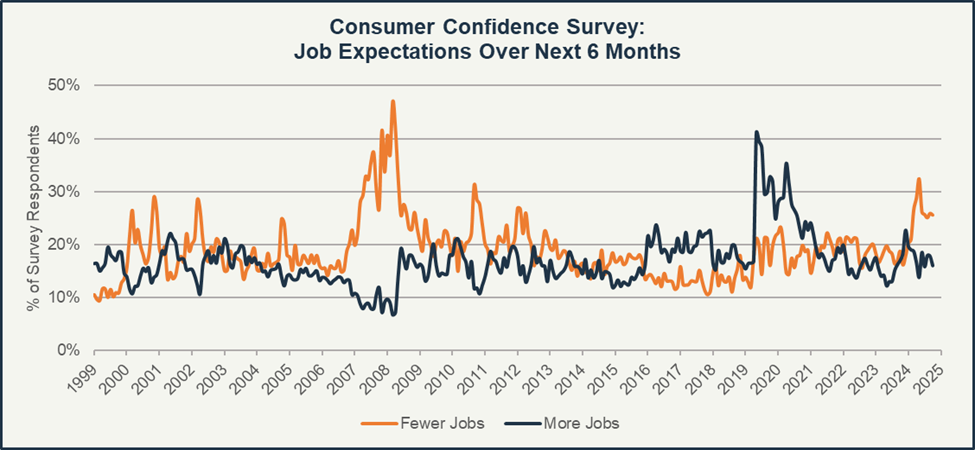

Not surprisingly, consumers’ feelings toward the job market are mixed and often stratified across income levels. However, given elevated levels of economic uncertainty, Conference Board survey participants increasingly see a tough labor market with fewer jobs available over the next six months.

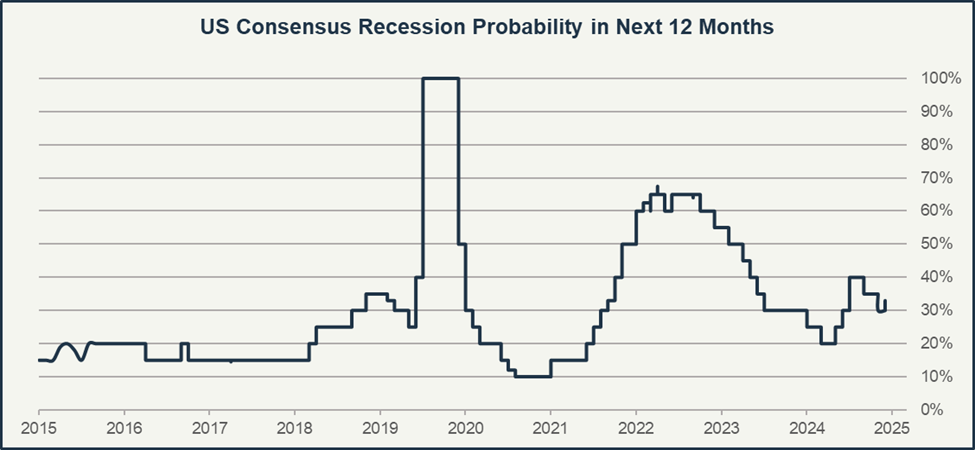

Among economists and strategists, the anticipated likelihood of a recession occurring in the next 12 months has declined from recent highs yet remains elevated compared to pre-Covid complacency.

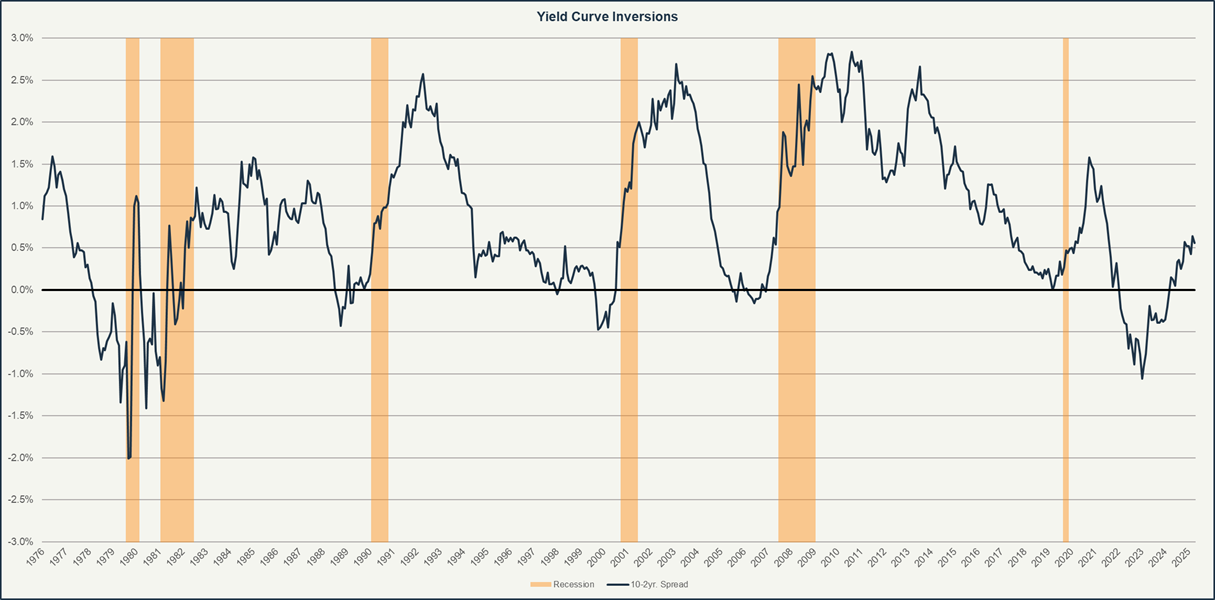

As we noted in our Fall 2024 Insights, the yield curve has continued to normalize, with short-term Treasury rates in particular declining in sympathy with lower Federal Reserve policy rates. The spread between 10yr. and 2yr. Treasuries—an oft cited recession indicator—has continued to widen, suggesting some sign of relief.

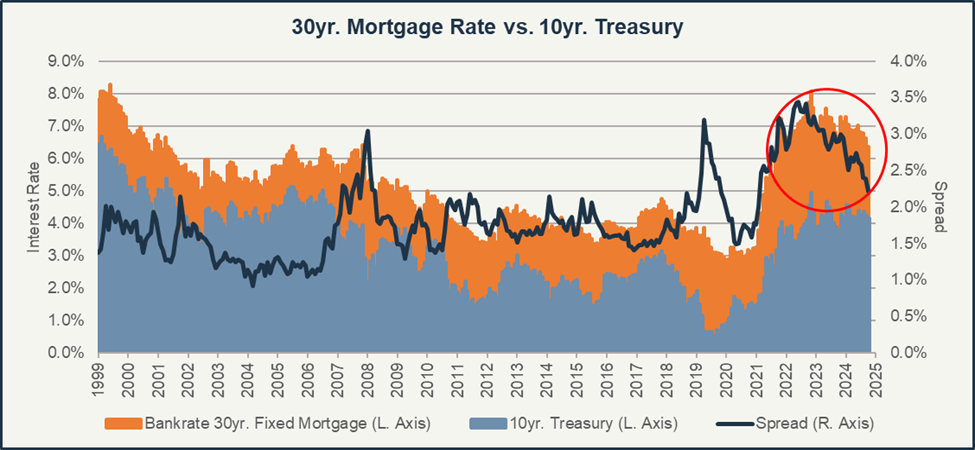

That said, a broader easing of interest rates—a much-broadcasted policy goal of the Trump Administration—has primarily been felt at the “shorter” end of the curve, while longer-term rates remain higher. This may be most relevant for consumers in the context of mortgages, which are more closely related to the 10yr. Treasury rate than short-term policy rates (i.e. the Fed Funds Rate). As a result, significant relief for current and prospective homebuyers has yet to materialize. However, the spread between the average 30yr. fixed mortgage rate and the 10yr. Treasury has begun to narrow, potentially signaling some improvement in the housing market and continued strength in homebuyer creditworthiness.

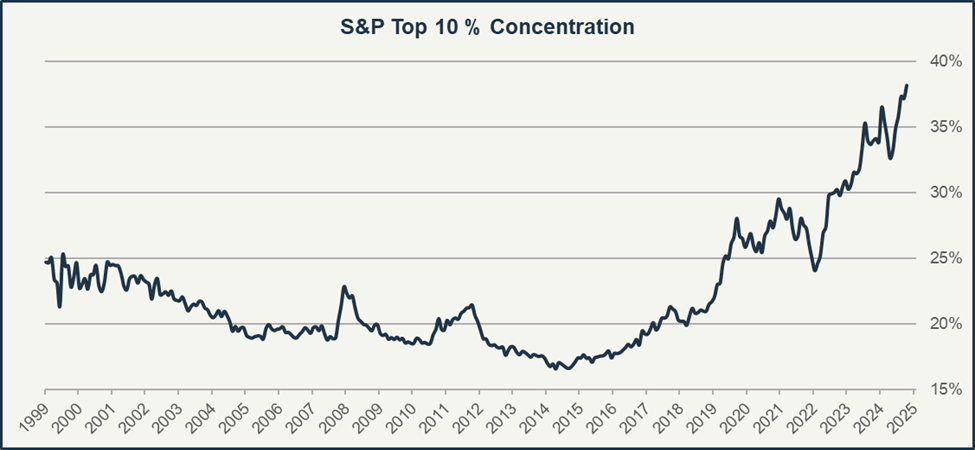

Last but not least, concentration within the S&P 500 remains at record highs. As we highlighted in our Summer 2023 Insights, a lack of “breadth” among equities is concerning for a few reasons. For one, those invested directly in the index (say, through an ETF) are likely taking on much more risk than is immediately apparent. With just the largest 10 names in the S&P accounting for nearly 40 percent of the entire index, the diversification benefits granted by the other 490 names are substantially muted. Further, the index’s headline performance—and that of the many funds and products tied to it—increasingly depends on the continued momentum of a handful of stocks, many of which are showing signs of fatigue after months (if not years) of unrelenting gains.

At the same time, the disconnect between the largest and smallest stocks in the S&P 500 may create opportunity for discerning investors and stock pickers. Active and conscientious portfolio management will be paramount going forward, particularly when—not if—the tide goes out for the tech “darlings” that have carried so much of the S&P’s recent momentum.