Push-Pull

Monetary policy is not a panacea.

Ben Bernanke

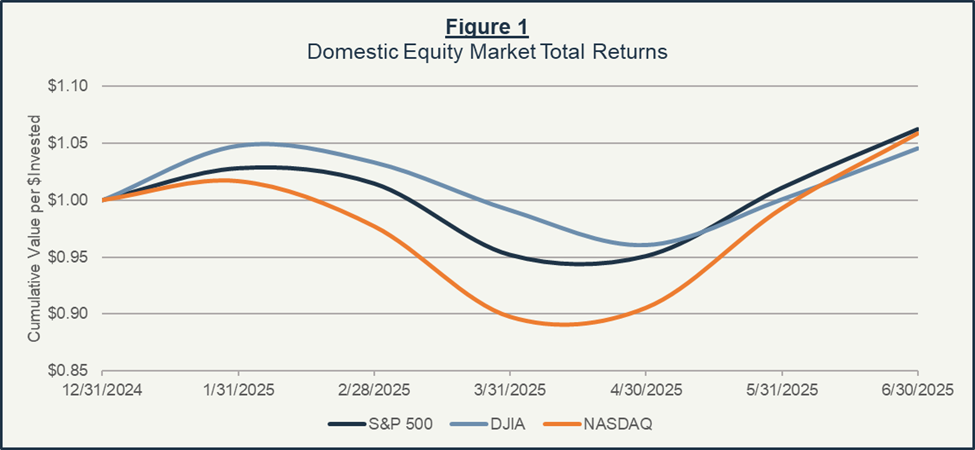

It is difficult to believe that, given how the second quarter of 2025 began, equity markets would find themselves at new all-time highs1 to close it out. Yet, such is the nature of volatility these days, further exemplifying the importance of the kind of patient, level-headed investing we espoused in our first quarter Insights. Once again faced with “unprecedented” levels of uncertainty (this time in the form of tariffs), investors that may have stepped to the sidelines amid early April market routs likely missed much of the recovery that quickly followed. In the end, the S&P 500 managed to deliver its best second-quarter performance since the pandemic (and the third best of the last 20 years), closing up 11%. The often more volatile Nasdaq produced even loftier quarterly gains of 18%, while the Dow delivered a comparably modest 5.5% total return.

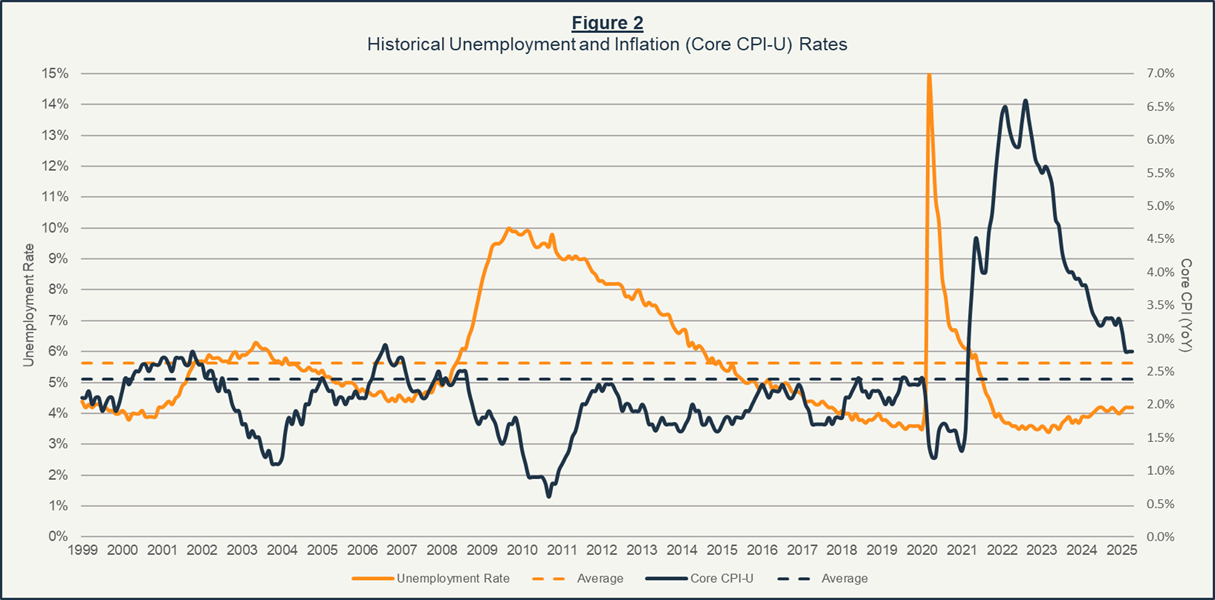

That said, when closely examining the relative strength of underlying economic conditions, maybe stocks’ Q2 outperformance should not come as much of a surprise. After all, market participants have historically proven largely adept at weighing “what ifs” against hard facts. Though sifting through headlines and various economic reports is no easy task, scrupulous investors would find some bright spots amid all the noise, including a “balanced” labor market2 with well-below-average unemployment and continued job growth, as well as inflation that remains generally in-line with long-term expectations and down significantly from recent peaks (Figure 2).

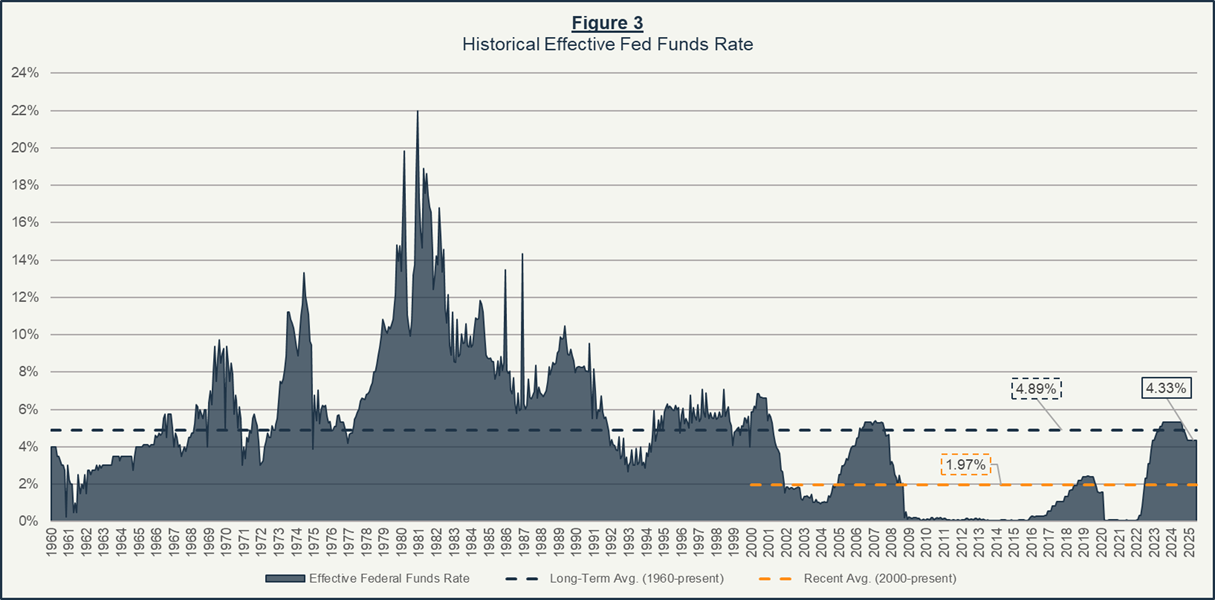

These factors are also generally supportive of the US’s current monetary policy regime—that is, the short-term interest rate policies set by the Federal Reserve that partly influence bond yields, loan rates, and other financial instruments. Despite much commentary to the contrary, the case for the Fed—an independent entity not technically governed by either the executive or legislative branches—to lower interest rates further3 is not straightforward. While the Fed’s key policy rate—known as the Effective Federal Funds Rate—remains elevated relative to recent history, interest rates still trend below the long-term average (Figure 3).

Viewed by some pundits and politicians to be restrictive, the Fed’s current stance stands in contrast with much more accommodative fiscal policy—that is, the federal government’s tax and spending regimes that influence the broader economy. Given the fresh wave of tax cuts, incentives, and higher levels of government spending embedded in the Trump Administration’s “One, Big, Beautiful Bill,” the Fed has struck a more cautious tone in order to avoid adding to factors that have the potential to reignite inflation. As we detailed in our Summer 2024 Insights, Fed rate cuts can be useful in encouraging consumer and business spending, which in turn injects capital into the economy and supports growth. However, too much capital flowing into the economy at the wrong time can also drive inflation higher and, if the economy subsequently slows, can create an insidious condition known as “stagflation,” whereby economic growth stagnates and unemployment and inflation rise simultaneously.

A basic explanation holds that supply shocks—such as a sharp increase in commodity prices—as well as government policies that hinder output while expanding the money supply too rapidly, both push an economy toward stagflation, which can be challenging to reverse. Though undertaken to correct a perceived trade imbalance, the implementation of tariffs (particularly those on a broad level) alongside otherwise stimulative fiscal policy risks such an outcome. Any additional stimulus in the form of lower interest rates might only exacerbate the situation, which is why Fed Chair, Jerome Powell, has directly cited tariff uncertainty as a reason why the Fed may maintain their current policy rate longer than previously expected. In the end, however, that may be the “medicine” needed to keep the economy on course while trade and tax policies continue to evolve.

_________________________________________________________________________________________

1 Both the S&P 500 and Nasdaq set record closing highs on June 30, 2025, while the Dow Jones Industrial Average fell just short of its all-time high from December 2024.

2 Quoting Federal Reserve Chair, Jerome Powell, from his June 2025 Federal Open Market Committee (FOMC) meeting press conference: “In the labor market, conditions have remained solid… Overall, a wide set of indicators suggests that conditions in the labor market are broadly in balance and consistent with maximum employment.”

3 The Fed initiated a brief “easing” cycle in late 2024 that saw its target rate lowered by 100 basis points, or 1%.