The 2026 Economic Outlook

The big money is not in the buying and selling, but in the waiting.

Charlie Munger

Each year, Merriam-Webster, the oldest dictionary publisher in the US, declares a “Word of the Year,” typically reflecting a major societal event or theme or a newly popular entrant into the common vernacular. For 2025, the choice was slop—that is, “digital content of low quality that is produced usually in quantity by means of artificial intelligence.” Undoubtedly, slop is of particular relevance (and concern) in today’s cultural and investment landscape, though another term also comes to mind when attempting to summarize 2025’s market performance: resilience.

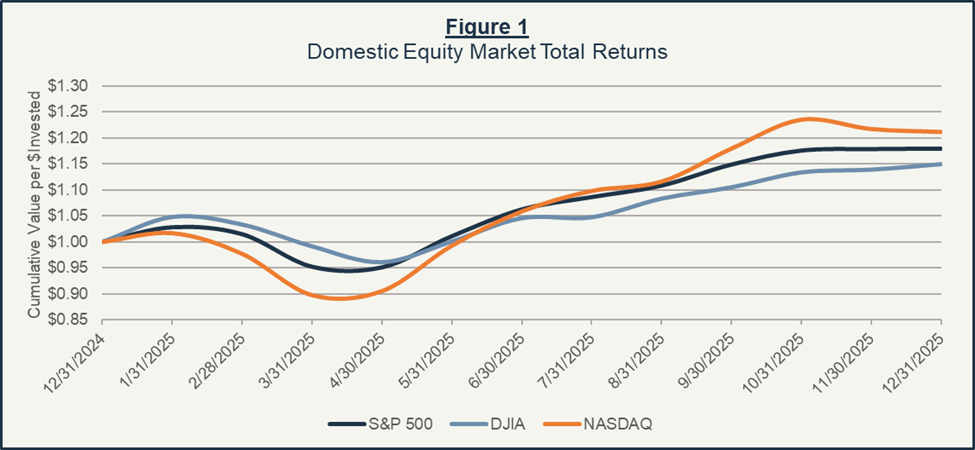

What began as a relatively lukewarm year for the S&P 500—down just over 2% in the first quarter—quickly accelerated into a sharp correction in early April as a flurry of trade and other fiscal policy shocks hit headlines. However, with the S&P still down some 14% from highs, our mid-April Insights newsletter urged a calmer, more patient mindset, arguing that a recovery could materialize swiftly and suddenly. And then it did.

In less than a month, the S&P had regained all of the ground it had lost since the start of the year, and by the end of the second quarter, the index had hit an all-time high. In fact, the S&P hit new all-time highs throughout each month of the second half—save for November—closing out 2025 just shy of a record 6,900, up ~18% from the end of 2024 (S&P 500 +17.9%; DJIA +14.9%; Nasdaq +21.1%).

Going into 2026, the year ahead looks primed for additional growth, albeit at a potentially moderated pace. The market will have to contend with lingering fiscal policy issues and continued monetary policy uncertainty as the Federal Reserve moves to balance rate cuts with inflation, while also simultaneously navigating the end of Chairman Jerome Powell’s term. But with solid GDP growth and relatively tame inflation in the cards, the stock market may enjoy continued tailwinds.

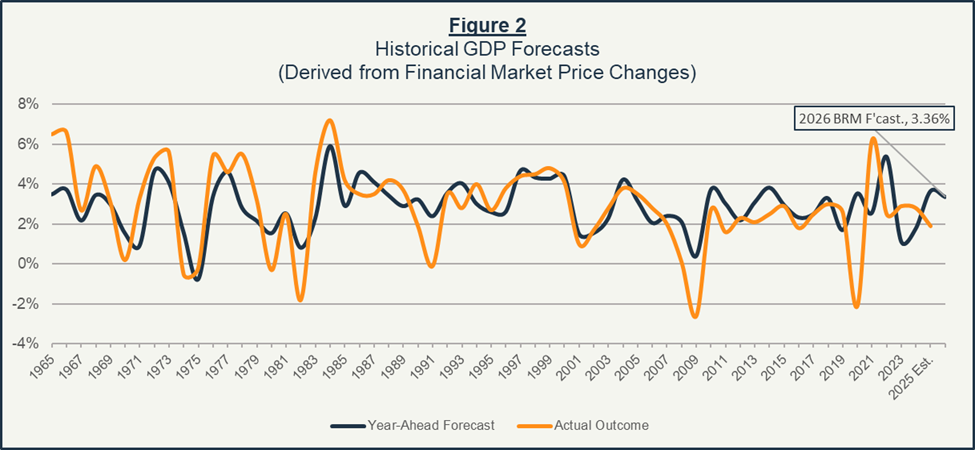

Beginning with economic growth (as measured by Gross Domestic Product), tax cuts either created or extended by the One Big Beautiful Bill (OBBB) should support consumer spending and domestic production, with provisions like exemptions on tipped and overtime income and expanded deductibility of research and development costs viewed favorably by economists. Modestly lower interest rates could also drive incremental growth, a factor partly embodied in our 2026 GDP Forecast shown in Figure 2. That said, robust economic conditions may discourage the Federal Reserve from lowering their key monetary policy rate—the Fed Funds Rate—any further, which could keep broader interest rates more rangebound than some would prefer.

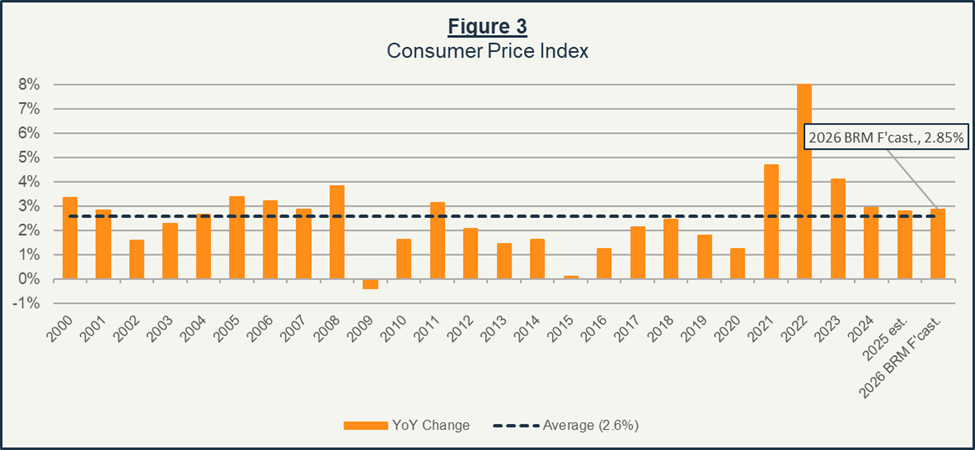

When it comes to inflation, there is optimism that the impact of the Trump Administration’s tariffs on consumer prices may peak in the first quarter of 2026. Pricing pressures could therefore recede as the year goes on, allowing continued wage growth amid stable employment to outpace inflation and further bolster household finances. Altogether, our model shown in Figure 3 suggests inflation (as measured by the Consumer Price Index) should, net-net, hold relatively steady this year, a potential sign of relief that trade tensions will not have quite the devastating impact once feared.

If 2025 was defined by resilience, 2026 stands to be a year of strategic calibration as we adjust to new norms. While our digital world may be increasingly cluttered with slop, underlying economic fundamentals suggest a clearer path forward for disciplined investors. As the market potentially moves toward a more moderate pace of growth, the value of a long-term perspective has never been higher.